Estably Blog

Market commentary: Winners of the pandemic are correcting

February 1 | Market Commentary

Pandemic-winners are fluctuating

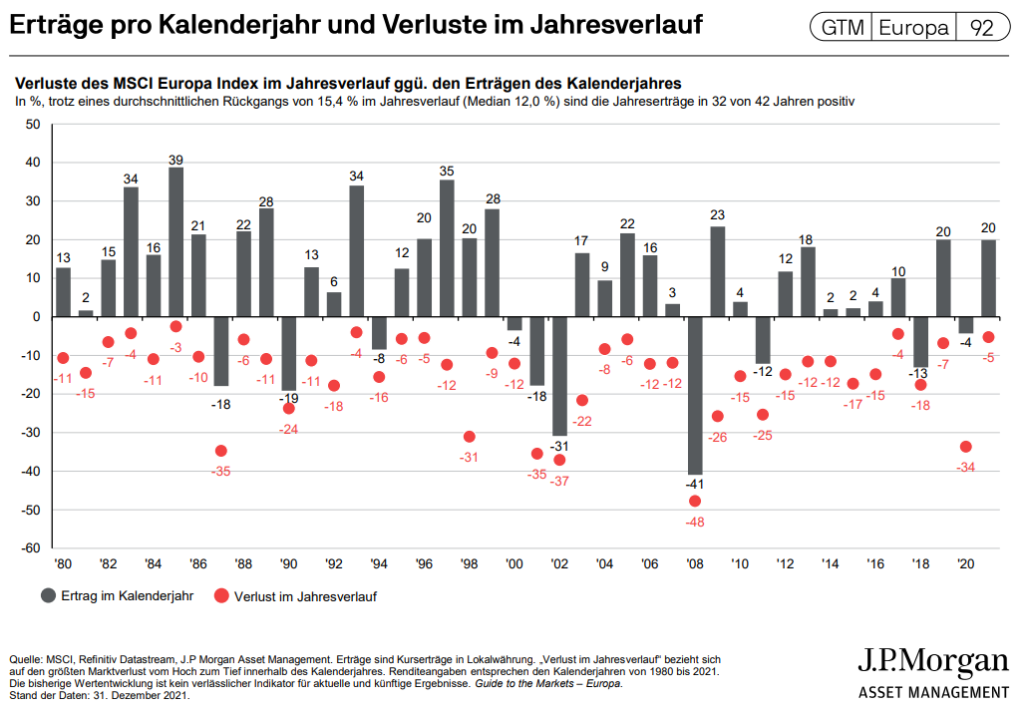

Setbacks during the year are completely normal

Rising interest rates are no threat to our technology companies

Don't try to be smarter than the masses

Conclusion

Estably is the first Liechtenstein-based digital asset management firm to offer world-class asset management through a blend of technology and human investment expertise. Thanks to the portfolio managers’ many years of experience in the field of value investing, the aim is to achieve above-average returns – starting at an investment sum of € 20,000. The aim is to make professional asset management, which was previously possible exclusively for major investors, accessible to everyone – in a convenient, transparent and profitable way.

You might also like these posts

Finance Blog

Half-year commentary 2023: From crisis to recovery

After a very turbulent 2022, the first half of 2023 saw a stabilisation in the capital markets, with strong recoveries in certain sectors.

Market commentary: Uncertainties lead to short-term price drops

Macroeconomic and geopolitical issues are resulting in uncertainties and leading to higher volatility on the capital markets.

Are Your Assets Protected From Financial Repression?

We live in a world where high government debt is the norm – not just since the COVID crisis.