Tips

The underestimated danger of financial repression

In troubled times, investors are looking for security for their assets. But what does “security” mean?

Tips

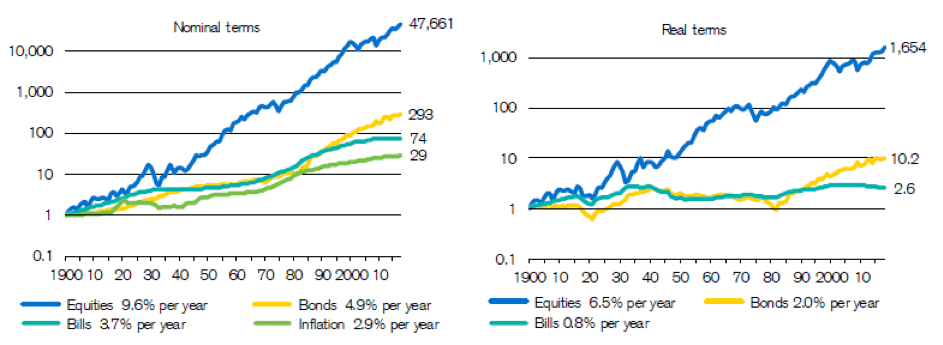

Speculators lose, long-term investors win

It’s no secret – those who invest in shares over a sufficiently long period of time achieve not only exclusively positive, but better returns than with bonds, precious metals, time deposits & Co.

Tips

What happened in March ’19?

The first quarter of 2019 is already over again and the worries from quarter 4 of 2018 seem to have long been forgotten. What else happened in march?