Estably Blog | Tipps

Create an inheritance:

Your financial roadmap for a carefree future

Published on 08.08.2024

For many people, a sudden inheritance means an unexpected windfall. Most family members have not thought about what to do with their inheritance beforehand. Today’s article is therefore intended to provide interesting facts and valuable tips on the topics of inheritance, taxes and the best investment options.

The most important facts in brief:

- In 2023, there were over 133,000 inheritances in Germany alone

- Germans inherit around €79,500 on average

- An inheritance of €100,000 or more is considered a “large inheritance“

an inheritance is taxed by the state like any income (but there are allowances!) - with inflation of over 5.90 % last year, the estate should be invested as profitably and sustainably as possible

An inheritance is more than just assets – it is the echo of past lives that opens up new paths for us. In the silence of transition lies the challenge of transforming memories into a meaningful future. And so heirs often also bear the responsibility of dealing sensibly and sustainably with their hard-earned inheritance. They are often spoilt for choice: park it in a savings account? Pay off debts or invest for a high return? Dealing with an inheritance is certainly just as exciting as its preservation and tax treatment.

In this article, you can find out more about the path to an inheritance, when and how you receive it and how best to invest your inheritance. Find out more about the following topics:

Contents

- 1 The great opportunity of an inheritance

1.1 What are the first steps after inheritance?

1.1.1 Valuation

1.1.2 Co-heirs

1.1.3 Inheritance tax

1.2 When and how do I receive my inheritance?

1.3 What are my (financial) goals with the inheritance? - 2. what is the best investment strategy for assets from an inheritance?

2.1 Traditional methods (savings accounts & call money)

2.2 High-yield options (shares, ETFs & funds) - 3. invest your inheritance yourself or get advice from professionals?

- 4 Our most successful portfolios for your inheritance money

4.1 Modern Value

4.2 Best of Funds

4.3 Asset Protect - 5 Conclusion: Invest your inheritance cleverly in different asset classes with Estably

Don't miss any more blog posts?

Subscribe to our newsletter NOW

1. The great opportunity of an inheritance

An inheritance is a great opportunity that can open many doors. It offers the opportunity to achieve financial security and realise long-cherished dreams. Heirs can use their assets to positively influence their lives and those of their loved ones.

"Inheritance is the beginning of a new financial journey."

And so the following wishes and plans are most often realised with the inheritance:

- Pay off debts: Many heirs use the assets they receive to pay off existing debts and thus improve their financial situation.

- Buying or renovating property: Inherited capital is often invested in the purchase of a property or an existing property is renovated.

- Education and further training: To finance a good education or further training for themselves or their children.

- Travelling and experiences: Some heirs fulfil long-cherished travel wishes or special experiences that they could not previously afford.

- Retirement provision: The inheritance is invested in retirement provision products to provide security for the future.

- Saving and investing: Heirs often put some of their assets into savings accounts or invest them in shares, ETFs, funds or other high-yield investments.And what is most often inherited? Interestingly, a survey conducted by the Berliner Morgenpost in 2023 found that Germans most frequently inherit money (75.2%) and, by a wide margin, owner-occupied property (29.8%), or securities accounts with shares and other securities (12.8%), but in the worst case also debts and liabilities (4.3%). In the latter case in particular, you can and should disclaim the inheritance.

Now the question arises: How exactly does an inheritance work, what does the statutory succession mean and what influence does a will have? In the following sections, we will therefore take a detailed look at the first steps after an inheritance and show you how you can receive and protect your inheritance.

1.1 What are the first steps after inheritance?

An inheritance has been received and you are suddenly faced with important decisions. What happens now? The first steps are crucial: from the valuation of the estate to legal questions about inheritance law and inheritance tax to clarification with co-heirs. We will guide you step by step to your inheritance:

- Obtain death certificate

- Apply for a certificate of inheritance

- Have your will checked

- Draw up an inventory of the estate

- Valuation of the estate

- Determination of heirs

- Observe statutory deadlines

- Submitting an inheritance tax return

- Obtain legal advice

- Carry out asset transfers

You should pay the most attention to the points “Valuation of the estate”, “Determination of heirs” and “Inheritance tax”, which is why we would like to go into these in more detail below.

1.1.1 Evaluation

The valuation of an inheritance includes money, tangible assets and liabilities. The value at the time of inheritance is decisive for inheritance tax and distribution. For capital in accounts, the valuation is clear; for shares, the prices on the date of death count. Tangible assets such as jewellery or real estate often require expert opinions or comparative values. Debts reduce the estate value. Heirs should draw up a precise statement of assets in order to obtain a clear picture of the inheritance and to correctly determine possible compulsory portions and tax burdens.

1.1.2 Co-heirs

When an inheritance is due, the question often arises as to who else is entitled to the estate. Firstly, you should check whether a will or contract of inheritance exists, as these documents can clearly regulate the succession. If there is no such regulation, the statutory succession comes into force. In this case, the German Civil Code (BGB) determines who is eligible as a co-heir. First-degree relatives, such as children and spouses, generally take precedence.

If the deceased leaves no direct descendants, relatives in the second degree also come into play. A precise examination of the statutory succession and the clarification of possible inheritance claims of co-heirs are therefore essential in order to distribute the estate correctly.

1.1.3 Inheritance tax

Sections 15 and 16 of the Inheritance Tax and Gift Tax Act (ErbStG) initially regulate the tax-free amounts, within the limits of which no inheritance tax is payable:

- Spouses and registered partners: €500,000

- Children and stepchildren: €400,000

- Grandchildren whose parents are deceased: 400.000 €

- Grandchildren whose parents are still alive: €200,000

- Great-grandchildren, parents and grandparents: €100,000

- Siblings and their children: €20,000

- Step-parents, children-in-law and parents-in-law: €20,000

- Divorced spouses and separated partners: €20,000

- All other heirs: €20,000

Inheritance tax is calculated according to tax class for all inheritances above the applicable tax-free amounts (tax class I: e.g. spouse and children, tax class II: e.g. more distant relatives such as siblings, tax class III: all others who are not related to the deceased).

Our personal tip for you:

“Alternatively, use gifts during your lifetime to save tax. Thanks to the tax-free allowances that apply every ten years, you can transfer assets (shares) tax-free. This means that the money can be invested by the donee (potential heir) for the long term and with a high return, while you significantly reduce your tax burden. At Estably, we offer you a wide range of attractive investment options and will be happy to present them to you free of charge and without obligation!”

Estably Asset Management AG

Schaanerstrasse 29

9490 Vaduz

Liechtenstein

Curious about personalized advice and tailor-made strategies for your individual situation? Get your free and non-binding initial consultation with us now!

1.2 When and how do I receive my inheritance?

The inheritance itself is received after the estate has been determined and valued and the order of succession has been clarified. Once all the formalities, such as applying for a certificate of inheritance and settling any debts, have been completed, the inheritance is distributed. This usually takes several weeks to months. Depending on the type of inheritance, payment is made by bank transfer, transfer of property titles or the transfer of tangible assets.

1.3 What are my (financial) goals with the inheritance?

From the heirs’ point of view, it can make sense to first seek comprehensive advice on what to do with the inheritance. For example, before you invest your inheritance yourself, you should seek holistic advice to understand the best options. Consider how the capital can best be invested to achieve your life goals. Whether for security, growth or to fulfil personal dreams, sound financial planning will help you use your inheritance wisely and effectively and avoid costly missteps.

2 What is the best investment strategy for assets from an inheritance?

Not all inheritances are the same. While some people are happy to receive an unexpected windfall, others are faced with the challenge of managing property or securities accounts. Cash can fulfil immediate wishes or be invested wisely to provide long-term security. Securities accounts require strategic management to ensure a stable income.

"Legacy well invested creates prosperity for generations"

The right decision on how best to invest the estate depends on many factors. Cash, account assets and money from the sale (of property or other valuables) can be invested either traditionally or with a high yield. The following subsections examine both options in more detail.

2.1 Traditional methods (savings accounts & call money)

Traditional methods such as savings accounts and call money offer safe but low returns. They are ideal for short-term goals or as a nest egg as they are easily accessible and low risk, but offer little growth potential. Estably offers attractive call money and fixed-term deposits (depending on the currency) specifically for this investment strategy.

| Währung | Callgeld | 1 Monat | 3 Monate | 6 Monate | 12 Monate |

|---|---|---|---|---|---|

| EUR | 1,68% | 1,84% | 1,95% | 2,17% | 2,34% |

| CHF | 0% | 0% | 0% | 0% | 0% |

| USD | 3,05% | 3,17% | 3,30% | 3,47% | 3,63% |

| AUD | 3,65% | 4,02% | 4,18% | 4,21% | 4,26% |

| CAD | 1,55% | 1,81% | 1,90% | 1,91% | 2,07% |

| NOK | 3,55% | 3,90% | 4,12% | 4,20% | 4,32% |

| GBP | 3,05% | 3,44% | 3,56% | 3,64% | 3,77% |

Figure 3: Our current overnight and fixed-term deposit interest rates by currency

However, there is a risk that inflation will exceed the achievable returns, causing the real value of money to fall in the long term. Last year, for example, inflation in Germany was 5.90 %, meaning that investors in traditional forms of saving would have suffered losses in real terms.

2.2 High-yield variants (shares, ETFs & funds)

High-yield options such as shares, ETFs and funds offer significantly higher profit opportunities. Shares represent shares in companies and can generate a considerable profit if they perform well. ETFs (exchange-traded funds) are exchange-traded funds that replicate entire market indices and thus offer broad diversification. Finally, investment funds pool the capital of many investors, which is invested in various securities by professional managers in order to spread the risk and achieve attractive returns at the same time.

On average, all three asset classes deliver returns that are higher than inflation. However, they are riskier and require a certain risk tolerance (which can vary from person to person).

Our personal tip for you:

“Estably’s strategies are an excellent choice as they minimise individual risk through professional management and broad diversification. Attractive returns can be achieved over longer investment periods despite market fluctuations. For you as a potential investor, this also has the advantage that you receive a comprehensive all-round service for the management of your capital from the inheritance and can invest it in an inflation-proof and sustainable manner. We would be happy to discuss this with you!”

Estably Asset Management AG

Schaanerstrasse 29

9490 Vaduz

Liechtenstein

Curious about personalised advice and tailor-made strategies for your individual situation? Get your free and non-binding initial consultation with us now!

3. invest your inheritance yourself or seek professional advice?

You have two main options when dealing with your inheritance: Invest yourself or seek professional advice.

If you choose self-management, you have full control and flexibility over your investments, but you need time and expertise to make informed decisions.

Alternatively, professional advice from experienced financial experts (for example, through Estably) can help you make the most of your inheritance by developing customised investment strategies and guiding you through complex markets. Professional advisers not only offer extensive knowledge, but also access to exclusive investment products and strategies. What’s more, an expert will also have a few financial tips for you.

The advantages of the second option are obvious:

- Expertise and experience: We bring extensive knowledge and years of experience in investment advice, which leads to more informed decisions.

- Customised strategies: We develop customised investment strategies that are tailored to your financial goals, risk tolerance and life situation.

- Access to exclusive products: We have access to investment products and strategies that are not generally available.

- Time saving: We take over the analysis and selection of investments for you, saving you valuable time.

- Risk management: We help you to identify and minimise risks in order to protect your capital.

- Market knowledge: You stay informed about market trends and economic developments.

- Regular review: We regularly monitor your investment strategy and adjust it if necessary to optimise your goals.

4 Our most successful portfolios for your inheritance money

When it comes to investing your inheritance in the best possible way, Estably offers you a range of proven strategies, each tailored to different types of investors and objectives. Whether you’re looking for high returns through targeted investments, consistent growth through diversified funds or maximum security through physical gold, each strategy offers unique benefits. Below we present our three most successful investment strategies, which are characterised by their individual approaches and objectives:

- Modern Value Strategy

- Best of Funds Strategy

- Asset Protect Strategy

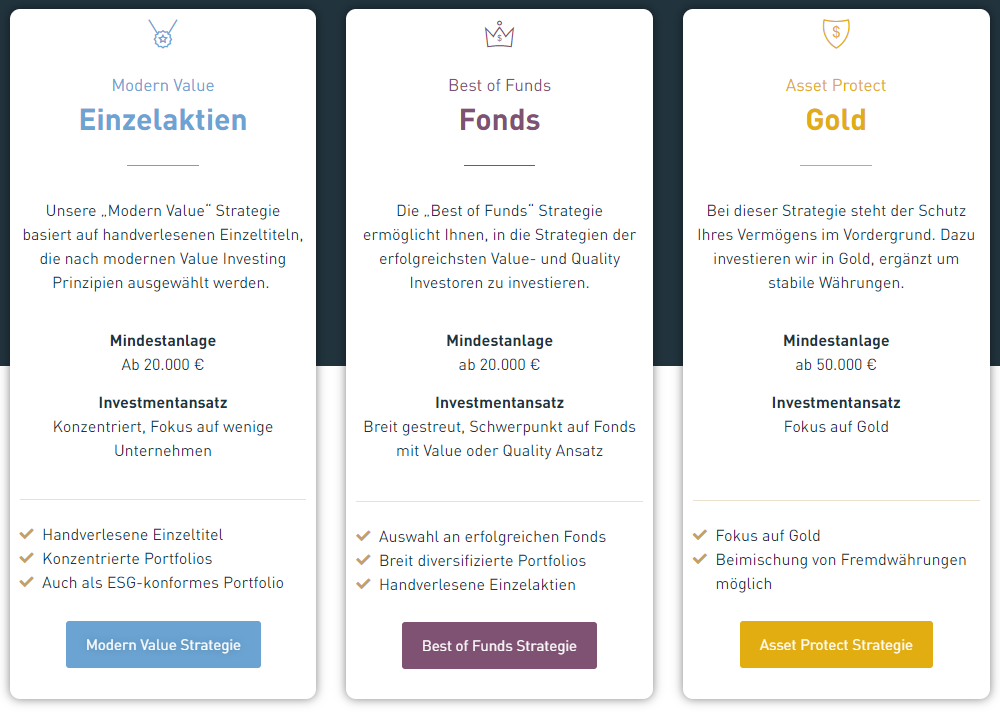

4.1. Modern Value

Our ‘Modern Value’ strategy offers you access to actively managed portfolios consisting of hand-picked individual stocks selected according to modern value investing principles. Specifically, this involves 20 to 25 individual stocks from the e-commerce, finance, services, pharmaceutical, technology and industrial sectors. Depending on the chosen strategy, an additional bond and cash component is added to the equity component, which is represented by our own Fructus Value Capital Funds. There are a total of five portfolios to choose from: Modern Value 20, 40, 60, 80 and 100 (where the number reflects the equity portion and the remaining portions are topped up by bonds and cash).

Benefit from the following additional advantages with Modern Value:

- your own securities account with Baader Bank or Liechtensteinische Landesbank

- No commitment or cancellation periods

- Access to your personal dashboard

- Regular information in the form of summarised quarterly reports and company updates

- Also available as an ESG-compliant Value Green strategy

- Possible from a minimum investment of just € 20,000

- Fair & transparent costs

4.2. Best of Funds

In turn, our ‘Best of Funds’ strategy enables you to benefit from the proven investment strategies of the most successful value and quality investors. With this strategy, we invest your assets in leading value and quality funds on a broadly diversified basis and supplement the portfolio with hand-picked individual shares of holding companies and actively managed bond funds. This diversification offers you a balanced risk/return profile and reduces fluctuations compared to concentrated individual share portfolios. Five different strategies are also available to you here: Best of Funds 20, 40, 60, 80 and 100.

Secure the following unbeatable advantages with ‘Best of Funds’:

- Your own securities account with Baader Bank or Liechtensteinische Landesbank

- No commitment or cancellation periods

- Access to your personal dashboard

- Tax advantages through partial exemption

- Already possible from a minimum investment of € 20,000

- Fair & transparent costs

4.3. Asset Protect

Our ‘Asset Protect’ strategy offers you reliable protection for your assets in uncertain times by investing in physical gold. The precious metal is stored securely for you in the vaults of the Liechtensteinische Landesbank (LLB). Gold has proven itself as a ‘safe haven’, especially during crises and negative real interest rates, when alternative investments such as fixed-term deposits can lose real value. In addition to gold, we invest in the stable Swiss franc to further secure your assets. Use the following five ‘Asset Protect’ strategies: Asset Protect 20, 40, 60, 80, 100 (where the number describes the physical gold component).

The popular ‘Asset Protect’ strategy offers you the following advantages:

- Investment in physical gold (stored at the LLB)

- Long-term protection for your assets

- No commitment or cancellation periods

- Access to your personal dashboard

- possible from a minimum investment amount of € 50,000

- fair & transparent costs

Our personal tip for you:

“For example, invest a third of your inheritance in “Modern Value” for growth, another third in “Best of Funds” for broad diversification and use the remaining 30-40% for “Asset Protect” to hedge with physical gold. This strategy combines potential returns with financial security. Let us work with you to determine your individual investment profile and risk tolerance to develop a customised strategy for you!”

Estably Asset Management AG

Schaanerstrasse 29

9490 Vaduz

Liechtenstein

Curious about personalised advice and tailor-made strategies for your individual situation? Get your free and non-binding initial consultation with us now!

5 Conclusion: Invest your inheritance cleverly in different asset classes with Estably

Instead of parking money from an inheritance in savings accounts, it is therefore best to invest in high-yield options such as equity funds or diversify into physical gold and stable currencies with our “Asset Protect” strategy. With our in-house investment strategies, you can not only compensate for inflation, but also sustainably increase your financial security and realize long-held goals. You can rely on customized advice and choose a strategy that makes the most of your inheritance.

"Turn your inheritance into more than just capital - shape your future!"

Estably, based in Vaduz in the Principality of Liechtenstein, offers investors not only access to high-quality portfolios, but also to the attractive benefits of a stable and flexible financial Center. Recognized in prestigious publications such as Forbes, Focus Money and wallstreet:online, Estably offers private and institutional investors a wide range of first-class financial services. Not yet an Estably client? We look forward to getting to know you free of charge and without obligation!

Let us advise you on the topics of finance, asset management, capital investment and much more!

DO YOU HAVE ANY QUESTIONS OR SUGGESTIONS ON THE ABOVE TOPIC? OR WOULD YOU LIKE TO LEARN MORE FROM US?

Did you like the article? Share it!

About Estably

Estably is the first digital asset management company from Liechtenstein to offer first-class wealth management through a blend of technology and human investment expertise. Thanks to the portfolio managers’ many years of experience in the field of value investing, the aim is to achieve above-average returns. The aim is to make professional asset management, which was previously exclusively available to major investors, accessible to everyone – conveniently, transparently and profitably.